Economic development is the process of boosting a geographic region’s economic well-being and quality of life. According to the Reserve Bank of India, India’s economic growth rate has been gradually growing, with a forecast growth rate of 7.5% for the fiscal year 2022-2023. On the other hand, economic development programs are critical to sustaining this progress and ensuring that it benefits all segments of society.

In this blog, we will define economic development, why having a plan is crucial, the advantages of economic development, and the strategies for economic growth and development.

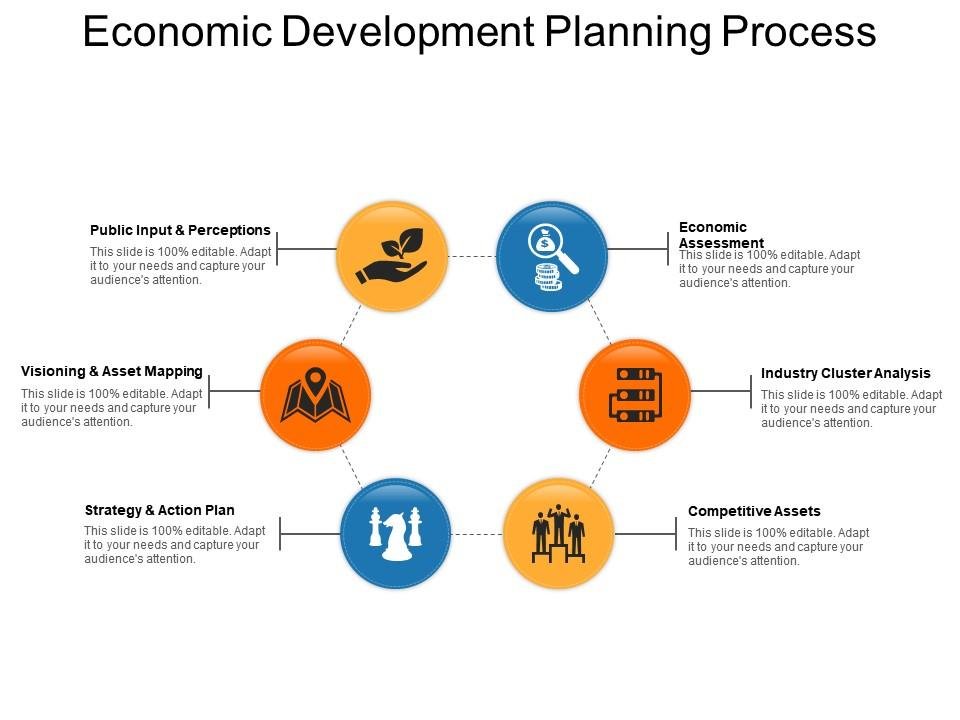

What is Economic Development?

Economic development is a process that aims to improve a given geographic region’s economic well-being and quality of life. It includes a wide variety of actions, including recruiting new firms and investments, expanding current businesses, generating employment, developing infrastructure, and increasing the region’s competitiveness. Economic development’s ultimate purpose is to provide long-term economic growth and development that benefits all segments of society.

Tax rebates, infrastructure development, labor training, and company support services are all examples of economic development projects. These measures can foster an atmosphere that encourages companies to prosper, attract new investment, and generate employment. Economic development is critical for a region’s long-term growth and sustainability because it fosters economic growth and job creation, improving citizens’ quality of life. Coordination of resources and stakeholders, alignment of goals, and identification of possibilities for growth and development are all required for effective economic development plans.

Why do you need to have an Economic Development Strategy?

Creating an economic development strategy is crucial for any region’s long-term prosperity and growth. Economic development activities can be disorganized, uncoordinated, and unproductive without a strategy. An economic development strategy lays a plan for economic growth and development, establishing objectives and identifying prospective growth prospects. It also aids in aligning stakeholders and resources, which is critical for obtaining the intended results.

A solid economic development plan is also essential for recruiting new enterprises and investment. It may foster a favorable business climate by offering incentives and assistance to enterprises, leading to job creation and increased economic activity. Moreover, economic development initiatives may boost a region’s competitiveness, improve its reputation, and increase investment and job creation. A well-planned economic development strategy may provide several benefits to an area, such as job creation, more tax income, and a higher quality of life for citizens.

Benefits of Economic Development

Economic growth is essential for a region’s well-being since it delivers several advantages to citizens and companies. Let us look more closely at the advantages of economic development:

- Job Creation: Creating new employment is one of the most significant benefits of economic progress. Economic development projects frequently center on recruiting new firms and investments in a region, which might create new employment opportunities. More work prospects can raise citizens’ living standards and lower unemployment rates.

- Increased Tax Revenues: Economic development may also contribute to a rise in the region’s tax revenues. Property, sales, and income taxes can grow when businesses expand and new ones come into existence. And businesses can utilize this extra money to support critical services and infrastructure initiatives.

- Increased Quality of Life: Economic progress may also enhance citizens’ quality of life. Increased household incomes can enhance access to education, healthcare, and other fundamental requirements due to the emergence of new work possibilities. Economic growth may also lead to the building of community facilities such as parks, recreational spaces, and community centers, which can improve inhabitants’ quality of life.

- Increased Entrepreneurship: Economic progress in a region may also contribute to increased entrepreneurship. Individuals may be more inclined to create their firms if the region becomes more business-friendly and attracts more investment. Entrepreneurship has the potential to provide new job opportunities, stimulate innovation, and boost economic growth.

Also Read about: Econometrics Assignment

What are the Best Practices for Economic Development Strategies?

Creating an efficient economic development strategy needs meticulous preparation and thought. It involves involving stakeholders, finding opportunities, and establishing priorities. Consider the following recommended practices when establishing an economic development strategy:

- Retention and Growth of Existing Businesses: Keeping and growing existing firms is an essential to economic development. This entails offering incentives and assistance to businesses in order to help them develop and flourish. Regions may create employment and boost economic activity by doing so.

- A Decent CRM Software: Good customer relationship management (CRM) software may be a significant economic growth instrument. It assists in tracking leads, managing contacts, and analyzing data, which may aid in identifying opportunities and tracking progress. A CRM system may also assist economic development professionals in staying organized and properly managing their workload.

- Align Important Stakeholders Around a Shared Vision: Successful economic development initiatives require key stakeholders to align around a shared vision. This entails bringing together players from the public and commercial sectors and developing a clear understanding of the region’s economic development objectives. Regions may achieve agreement and guarantee everyone is working towards the same goals.

- Keeping your Leadership on the Same Page: Effective economic development strategies require strong leadership and coordination. Maintaining oversight’s focus and ensuring that all parties are working towards the same goals are crucial. This is made feasible by using project management tools and processes, as well as ongoing communication and collaboration.

- Recognize and Develop Your Available Sites and Buildings: An area’s ability to expand economically depends on its ability to recognise and develop its available sites and structures. This approach includes finding underutilized or abandoned locations that could be renovated or repurposed to draw in new businesses and investment. By doing this, regions can increase their competitiveness and appeal to potential investors.